Rahul Sompuram — CEO & Co-Founder at OpenHand

Sep 25, 2024

Chances are you already know what a medical bill is but do you know what goes on behind the scenes? Let's break down the journey of a medical bill and translate some of that confusing jargon along the way.

Chapter 1: Your doctor’s visit

Your bill's adventure starts as soon as you receive care at the doctor's office. Here's what you might encounter:

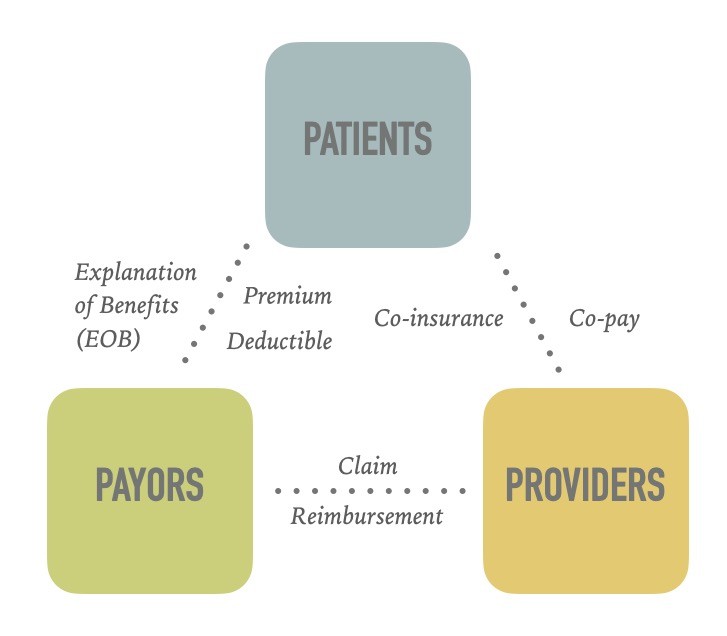

Premium: Even before you see the doctor, you might also be paying a monthly fee to keep your insurance active. It’s like a subscription that guarantees you’ll have coverage when you need it.

Deductible: This is a dollar threshold you need to hit each year before your insurance starts chipping in. Until you reach this amount, you have to pay on your own.

Co-insurance: Once you've hit your deductible, you and your insurance become a team. You might pay 20%, they pay 80% — it's a cost-sharing handshake.

Co-pay: Think of this as your ticket to see the doctor. It's usually a fixed amount you pay upfront, kind of like a cover charge at a club.

Self-pay: No insurance? You're solo here, potentially paying the full amount or arranging a payment plan.

It’s important to remember that these initial payments are often estimates. The final bill might look different after your insurance processes everything, kind of like how your online shopping cart changes after applying discounts and taxes.

Chapter 2: Turning your visit into codes and claims

After you leave, your doctor's office gets busy. They turn your visit into a series of diagnosis codes (i.e. ICD-10 codes) and procedure codes (i.e. CPT codes) that tell your insurance company what happened and ultimately determine what you’ll be charged for on the claim (i.e. the bill). It's like translating your visit into a secret language only billing departments understand.

This is where errors are most frequently introduced. There are so many different ways coding issues can show up, some unintentional and some…intentional (a story for another day):

Duplicate charges: The same service might accidentally be entered twice.

Upcoding: Sometimes a service might be coded as more complex than it actually was. It's like being charged for a gourmet meal when you ordered a deli sandwich.

Unbundling: This is when services that should be grouped together are billed separately, potentially increasing the cost.

Incorrect codes: Sometimes, the wrong code is used entirely.

And many more…

These errors are more common than you might think. The Medical Billing Advocates of America estimates that 80% of bills have errors. That’s like you giving out extra money every 4 out of 5 times.

Chapter 3: The payor & provider negotiation dance

Next, the hospital or clinic (i.e. the provider) sends a claim to your insurance company (i.e. the payor). They look at the codes and decide how much they're willing to pay. This process involves several steps:

Verification of eligibility: They check if you're covered and have an active membership.

Review of covered benefits: They see if the services you received are included in your plan. Think of it like checking if a feature is available with your basic subscription or if you need the premium plan to access it.

Application of allowed amounts: An allowed amount is the maximum they'll pay for each service.

Determination of payment: They decide how much they'll pay and how much you might owe.

What follows is a negotiation process between the payor and the provider that can take anywhere from a few days to several weeks, sometimes even escalating to arbitration. This back-and-forth is one big reason why healthcare costs can vary so much for the same services.

Chapter 4: The EOB, your bill’s sneak preview

After all the Shark Tank-esque negotiating, your insurance sends you an Explanation of Benefits (EOB). Here's the important part: An EOB is not a bill. It's more like an outline of what you’re about to owe to the provider.

Your EOB will usually show useful information like:

Service Description: What medical services you received. It might use terms like "venipuncture" (that's just a fancy way of saying they drew your blood).

Amount Billed: The original price the provider charged.

Plan Discount: The amount your insurance negotiated off.

Amount Paid: What your insurance covered (i.e. their portion of the co-pay).

Patient Responsibility: What you [might] need to pay.

Once you receive the actual bill from your provider, that’s when you’ll need to make any payments (or try to negotiate them down).

Chapter 5: Taking control of your bill

Now that you know how medical bills actually work, here are some steps that give you the power to better manage your healthcare costs:

Read your EOB: It might seem as dry as reading the terms and conditions, but it's your chance to spot any issues early.

Question unusual charges: If something doesn’t look right, don’t be shy about calling your healthcare provider or insurance company for clarification.

Know your insurance: Understanding your plan can help you avoid surprises.

Keep Your Paperwork: Save your bills and EOBs. They might come in handy later, like a receipt for a big purchase.

Negotiate: Thanks to new rules around price transparency, there’s almost always room to negotiate your medical bills down. We’ll dive deeper into the art of negotiating your medical bills in a future post.

Always remember that you have the right to understand your medical bills. If something doesn't make sense, question it. Investigate it. Negotiate it. With a little know-how, you can navigate the world of medical billing like a pro.